How do you convert a second home or vacation home into a 1031 exchange investment property? You must stop treating the property mainly as a personal-use home. You must begin treating it as an investment propert

That usually means you rent it at fair market rent. You also limit personal use, keep strong records, and plan before you sell.

This strategy could be important for owners of second homes and vacation properties in coastal Charleston markets. That includes Kiawah Island, Seabrook Island, Edisto Beach, Folly Beach, Sullivan’s Island, Isle of Palms, Daniel Island, and other Lowcountry communities.

Many of these properties have increased greatly in value. Because of that, owners may face a large capital gains tax bill when they sell.

A pure second home does not qualify for a 1031 exchange just because it is not your primary residence. To qualify, you must hold the property for investment or business use.

That is where many vacation homeowners get confused.

The good news is that some second homes and vacation homes can become investment properties. With the right planning, they may qualify for a 1031 exchange in the future.

Why a Personal-Use Second Home Does Not Qualify

A 1031 exchange applies to real estate held for investment or business use. It does not apply to a home used mainly for personal enjoyment.

If you use your beach house, island home, waterfront retreat, or Charleston-area vacation property mostly for family visits, weekends, or vacations, it likely does not meet the investment-use requirement.

Appreciation alone does not make a property qualify.

For example, a property on Kiawah Island, Seabrook Island, Edisto Beach, Folly Beach, Sullivan’s Island, Isle of Palms, or Daniel Island may have gained significant value. But value growth by itself does not turn a second home into a 1031 exchange property.

You need to create a clear investment-use history.

Step 1: Commit to Holding the Property as an Investment

The first step is changing how you use the property.

If you want to sell through a 1031 exchange later, start treating the property like an investment now. Make rental activity part of the plan. Limit personal use. Keep careful records.

This matters in vacation-home markets. Many owners mix personal use, family use, and rental income.

A property may feel like an investment because it produces some rental income. But occasional rental income does not automatically make it qualify for a 1031 exchange.

You should not wait until the property goes under contract to ask these questions. If you used the property heavily for personal reasons, you may need two years of planning before you sell.

Step 2: Rent the Property at Fair Market Rent

Under the vacation home 1031 exchange guidelines in Revenue Procedure 2008-16, you generally need to rent the property at fair market rent for at least 14 days in each of the two 12-month periods before the exchange.

You should charge real market rent. Do not rely on a discounted family rate or an informal arrangement.

For example, assume you own a vacation property on Folly Beach, Edisto Beach, Isle of Palms, Seabrook Island, or Kiawah Island. You should be able to show that your rental rate matches similar properties in that market and season.

Good documentation may include:

Rental agreements

Property management statements

Online booking records

Comparable rental data

Proof of rental payments

Tax records showing rental income and expenses

Your goal is simple. Show that you operated the property as a real investment.

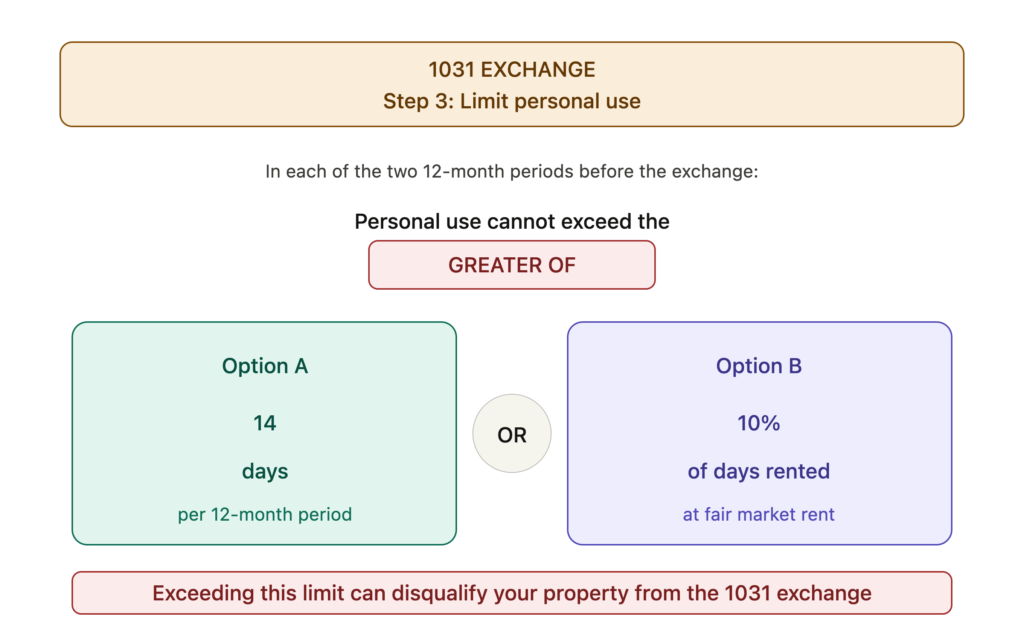

Step 3: Limit Personal Use

Personal use often creates the biggest problem.

In each of the two 12-month periods before the exchange, personal use generally cannot exceed the greater of:

14 days, or 10% of the number of days you rent the property at fair market rent.

Here is a simple example.

If you rent your vacation home for 200 days in a year, 10% equals 20 days. In that case, you may use the property personally for up to 20 days and stay within the limit.

But if you rent the property for only 100 days, 10% equals 10 days. Since the rule allows the greater of 14 days or 10%, your personal-use limit would generally be 14 days.

This is why occasional rental activity may not be enough.

Owners of second homes on Daniel Island, Sullivan’s Island, Kiawah Island, Seabrook Island, Edisto Beach, Folly Beach, and Isle of Palms should track both rental days and personal-use days.

If a future 1031 exchange is part of the plan, the numbers matter.

Step 4: Be Careful With Family Use

Family use can create unexpected tax problems.

Use by certain related parties may count as personal use, even if you charge rent. One major exception may apply. The related party must use the property as a primary residence and pay fair market rent.

That means vacations by children, siblings, parents, or other family members may count against your personal-use limit.

This issue comes up often with Lowcountry second homes. Families often treat beach and island properties as shared gathering places.

That may work well for the family. But it can complicate a future 1031 exchange.

If you want to convert the property into an investment property, handle family use carefully. Discuss it with your tax advisor before you create a problem.

Step 5: Keep Strong Records

Documentation matters.

If the IRS questions the exchange, you want clear records. You should save rental records, income records, expense records, booking history, and fair market rent support.

You should also track every personal-use day.

Strong records can help show that you held the property for investment.

This can be especially important in seasonal markets such as Edisto Beach, Folly Beach, Sullivan’s Island, Isle of Palms, Kiawah Island, and Seabrook Island. Rental rates and occupancy can change by season, so documentation becomes even more important.

Step 6: Talk to a Tax Advisor Before You List

You must structure a 1031 exchange before the sale closes. You cannot sell the property, take the money, and then decide to do a 1031 exchange later.

Before you list, speak with your CPA, tax attorney, and qualified intermediary.

Review the property’s rental history. Have you documented your personal-use history. Review your ownership period. Make sure the facts support the strategy.

This step matters even more with second homes and vacation homes because details can change the outcome.

Can You Convert the Replacement Property Back Into a Vacation Home Later?

Possibly.

If you exchange into another vacation rental or second-home-style property, you should also hold the replacement property for investment.

That usually means you rent it at fair market rent. You also limit personal use and document the investment purpose after the exchange.

Over time, your plans may change. You may later want to use the replacement property more like a personal vacation home.

That may be possible. But you should discuss the timing and tax impact with your advisors before you make the change.

For example, you may exchange out of a highly appreciated vacation property on Isle of Palms, Folly Beach, or Seabrook Island. Then you may buy another investment property that better fits your income, retirement, or estate-planning goals.

Later, your personal plans may change.

That flexibility may exist, but the investment-use rules need to come first.

You may be able to have flexibility, but not all at once. If tax deferral is the goal, follow the investment-use rules first.

Converting a Second Home into 1031 Exchange Property Key Takeaways

To convert a second home or vacation home into a property that may qualify for a 1031 exchange, start planning early.

Reduce personal use. Rent the property at fair market rent. Keep strong records. Treat the property like an investment.

For many owners in coastal Charleston markets, the opportunity may be real. That includes Kiawah Island, Seabrook Island, Edisto Beach, Folly Beach, Sullivan’s Island, Isle of Palms, and Daniel Island.

But timing matters.

If you own a second home or vacation rental in the Charleston area and are thinking about selling, review your options before you make a final decision.

Start with the basics. Discover what the property worth? What is the rental history? Is your capital gains exposure sgnificant? What replacement-property options could fit your goals?

Those questions can help you decide whether a 1031 exchange strategy deserves a closer look.

Important Disclaimer Regarding Converting a Second Home into 1031 Exchange Property

Bill Byrd and Waverly Byrd of the Byrd Property Group are real estate professionals. They are not tax advisors, attorneys, financial planners, or investment advisors.

This article is for general educational purposes only. It should not be considered tax, legal, financial, or investment advice.

1031 exchanges, capital gains taxes, depreciation recapture, second-home conversions, and related tax strategies can be complex. Your options depend on your specific facts and circumstances.

Before you sell, convert, or exchange real estate, consult your CPA, tax attorney, qualified intermediary, financial advisor, and other appropriate professionals.

Byrd Property Group can help you evaluate the real estate side of the decision. That may include market value, sale strategy, rental potential, timing, and replacement-property considerations.

You should make all tax, legal, and investment decisions with guidance from properly licensed professionals.

Convert a Second Home into 1031 Exchange Property – FAQ’s

Possibly. A pure second home does not qualify. But you may convert it into an investment property by renting it at fair market rent, limiting personal use, and documenting investment use over time.

The vacation home guidelines generally look at the two 12-month periods before the exchange. In each period, you should rent the property at fair market rent for at least 14 days.

Personal use generally should not exceed the greater of 14 days or 10% of the number of days you rent the property at fair market rent during each 12-month period.

Often, yes. Use by certain related parties can count as personal use, even if you charge rent. Some exceptions may apply, so speak with your tax advisor.

Start before you are ready to sell. If you used the property mostly for personal reasons, you may need time to build the rental and investment-use history needed to support a future 1031 exchange.

About the Authors

Bill Byrd and Waverly Byrd serve clients throughout the Charleston area as Real Estate Wealth Advisors, helping individuals and families navigate complex property decisions connected to life transitions and long-term planning. Their work often involves, tax-advantaged 1031 exchanges, probate and estate property sales, divorce-related real estate solutions, trusts, and senior relocation, situations where informed coordination and careful timing can significantly impact outcomes.

With decades of experience, Bill and Waverly emphasize education, clarity, and collaboration. They regularly work alongside financial planners, tax professionals, and attorneys to help clients understand their options and align real estate decisions with broader financial and estate planning goals. As a father-and-daughter team, they guide clients through sensitive transactions with discretion, organization, and a steady, well-informed approach across the Lowcountry.