A Strategic Tax Tool for Residential and Commercial Real Estate Investors

Wondering how Cost Segregation in the Charleston Area could dramatically reduce your tax burden increase your cash flow and accelerate portfolio growth?

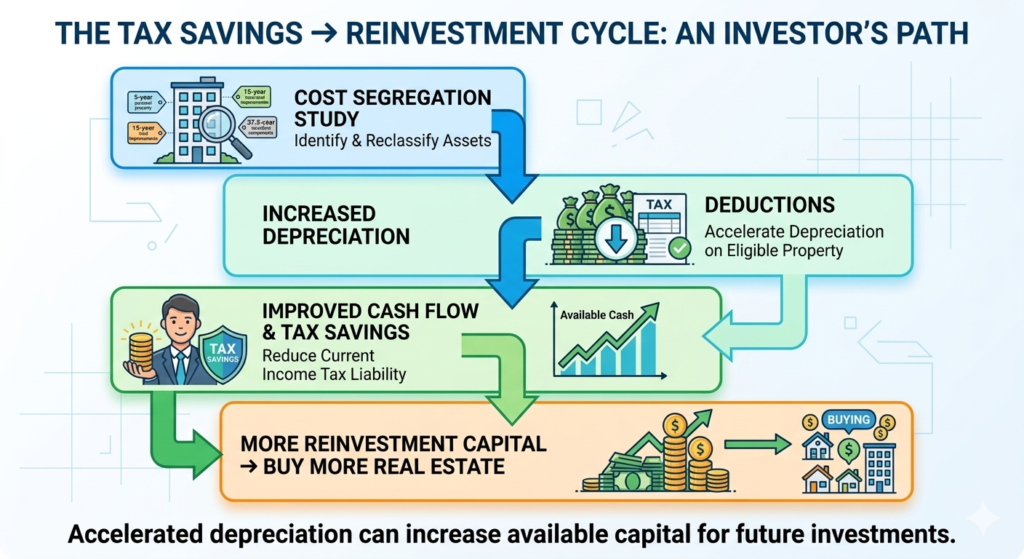

Cost Segregation allows you to accelerate depreciation on investment property, increasing early-year deductions and improving cash flow. When applied strategically, especially alongside bonus depreciation, it can free up capital to reinvest into additional properties or reduce overall tax exposure.

Introduction to Cost Segregation

If you own rental property in the Charleston Area, Cost Segregation is one of the most powerful tax planning tools available to you. In this post we are going to primarily focus on residential real estate.

Most investors depreciate residential rental property over 27.5 years (or 39 years for commercial property). That “straight-line” approach spreads deductions evenly across decades. It’s simple. It’s common. And in many cases, it leaves significant money on the table.

Cost Segregation uses an IRS-approved engineering methodology to break a building into separate and individual components. Some of of these qualify for accelerated depreciation over 5, 7, or 15 years instead of 27.5 or 39 years. When paired with bonus depreciation, those accelerated components may be deducted immediately.

For Charleston real estate investors navigating rising property values, evolving short-term rental rules, higher insurance costs, higher real estate tax, rising material and labor costs and strong long-term appreciation, this strategy deserves careful consideration.

What Is Cost Segregation?

Cost Segregation is an IRS-recognized depreciation strategy that:

- Breaks down a property into individual components.

- Reclassifies certain components into shorter depreciation lives.

- Accelerates tax deductions into earlier years of ownership.

Instead of depreciating the entire building over 27.5 years (residential) or 39 years (commercial), portions may qualify for:

- 5-year property (carpet, certain flooring, specialty lighting, appliances)

- 7-year property (certain equipment)

- 15-year property (site improvements such as landscaping, sidewalks, driveways, fencing)

These shorter-life components may also qualify for bonus depreciation.

This methodology has been supported by tax court decisions since the 1940s and remains fully recognized by the IRS. And, I’ve been told, the IRS actually prefers cost segregation over straight-line depreciation!

How Bonus Depreciation Works

Bonus depreciation applies to the components of a property with a class life of 20 years or less. That means:

- 5-year assets qualify

- 7-year assets qualify

- 15-year assets qualify

Under current law (including recent reinstatement provisions), qualifying property placed in service may benefit from 100% bonus depreciation in many cases.

That means qualifying components may be deducted in year one instead of spread over several years.

This is not a tax credit. It is an accelerated deduction.

Cumulative depreciation deductions over the first 10 years on a $1M commercial property. Cost segregation assumes 30% of assets reclassified to 5/7-year property with bonus depreciation applied in year 1.

How the components break down

| Asset class | % of value | Recovery period | Method |

|---|---|---|---|

| Personal property (fixtures, equipment) | 15–20% | 5 years | Accelerated / bonus |

| Land improvements (parking, landscaping) | 8–12% | 15 years | Accelerated / bonus |

| Building structure | 70–75% | 27.5 / 39 years | Straight-line |

For illustrative purposes only. Assumes 37% tax bracket, 100% bonus depreciation, and no passive activity limitations. Consult a qualified tax professional.

Cost Segregation Chart Explained

Here’s a quick breakdown of what the above chart illustrates:

The line chart shows cumulative depreciation deductions over 10 years on a $1M property. The big story is in year 1: cost segregation can deliver over $285,000 in deductions right away (assuming bonus depreciation), compared to just $36,364 under 39-year straight-line or $25,641 under 27.5-year. That front-loaded deduction is the core value proposition.

A few things worth noting:

Why the gap matters – earlier deductions mean earlier tax savings, and that freed-up cash can be reinvested. It’s a time-value-of-money play, not just a total deduction difference (the total depreciation over the life of the property is the same either way).

Bonus depreciation – the large year-1 spike assumes 100% bonus depreciation on the reclassified assets. Bonus depreciation has been phasing down (it was 80% in 2023, 60% in 2024), so the exact numbers will vary by year.

Who it works best for – investors with passive income to offset, or real estate professionals who qualify to use losses against ordinary income, get the most benefit.

Why This Matters in the Charleston Area

Charleston has experienced:

- Strong appreciation in residential investment property

- Growth in short-term rental activity (where permitted)

- Increased investor competition

- Rising construction and improvement costs

- Rising insurance costs

- Higher property taxes

- Pressure on rents in some micro markets in Charleston

Many investors are equity-rich but cash-flow constrained. Cost Segregation improves early-year cash flow without increasing rent or leverage.

This matters when:

- Acquiring new rental properties

- Converting primary residences into rentals

- Renovating older Charleston homes

- Purchasing small multifamily assets

- Acquiring beach-area short-term rentals (where legally permitted)

Strategically deployed, it can support reinvestment into additional Charleston area lowcountry properties.

Who Is a Good Candidate?

Cost Segregation may make sense if you:

- Own residential rental property

- Own small multifamily property

- Operate a short-term rental

- Have completed renovations exceeding $50,000

- Purchased property within the last 10–15 years

- Are involved in a 1031 exchange

- Inherited investment property with stepped-up basis

It may not make sense for:

- Fix-and-flip projects

- Primary residences not used as rentals

- Investors with substantial unused passive losses (without planning)

Each situation requires review and a consultation with your Accountant, Attorney, Financial Planner, your Real Estate Wealth Advisor and of course a Cost Segregation expert.

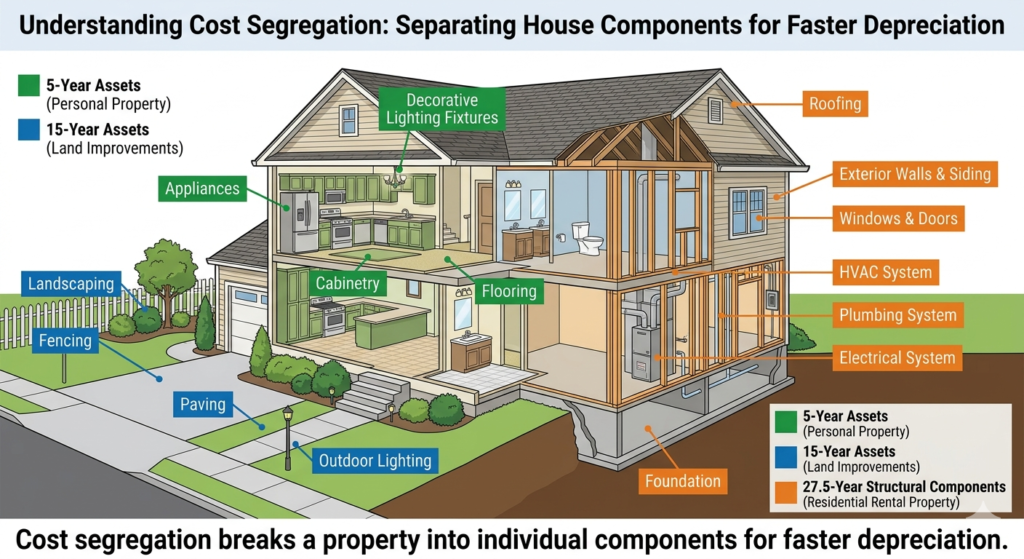

What Can Get Reclassified in a Residential Property Cost Segregation Study?

Short Answer:

A cost segregation study identifies building components that can be depreciated faster than the standard 27.5-year schedule used for residential rental property. Items such as cabinets, appliances, decorative lighting, specialty flooring, driveways, landscaping, and irrigation systems may qualify for 5-year or 15-year depreciation instead of being treated as structural assets.

One of the most common questions real estate investors ask is:

“What parts of a property actually qualify for accelerated depreciation?”

A cost segregation study examines a building in detail and separates the components that depreciate faster from the core structural elements of the property.

Instead of treating the entire property as a single 27.5-year asset, engineers identify specific elements that qualify for 5-year or 15-year depreciation categories, which may also qualify for bonus depreciation.

Below is a simplified example of how these components are typically categorized in a residential cost segregation study.

| Category | Examples |

|---|---|

| 5-Year Assets (Personal Property) | Kitchen cabinets, appliances, decorative lighting, specialty flooring such as floating hardwood or laminate, removable shelving, window coverings, certain plumbing fixtures |

| 15-Year Assets (Land Improvements) | Driveways, sidewalks, patios, landscaping, irrigation systems, fencing, outdoor lighting, retaining walls, pools, and other exterior site improvements |

| Structural Assets (27.5-Year Property) | Roof structure, framing, drywall, insulation, plumbing systems, HVAC systems, electrical distribution systems, and load-bearing building components |

Why This Matters for Investors

The assets identified in the 5-year and 15-year categories may qualify for accelerated depreciation and bonus depreciation. This allows investors to recognize a much larger portion of their tax deductions in the early years of ownership rather than spreading them evenly over nearly three decades.

In many residential rental properties, a cost segregation study may reclassify 20%–35% of the building value into these faster depreciation categories.

For Charleston investors, that acceleration can significantly improve early cash flow and free up capital for future acquisitions.

The Importance of an Engineering Study

A legitimate cost segregation study is not simply an estimate. Qualified engineering professionals typically analyze:

- Construction drawings

- On-site inspections

- Detailed cost estimates

- Quantity measurements of building components

This level of documentation helps ensure the study meets IRS standards and supports the accelerated depreciation classifications.

Because of this detailed process, the results often reveal hundreds of individual building components that can be categorized and depreciated more efficiently.

The Material Participation Question

Many Charleston investors ask:

“Can I use these deductions against my W-2 income?”

The answer may depend on:

- Real Estate Professional Status (750+ hours annually)

- Material Participation (especially for short-term rentals)

- Passive activity grouping elections

- Overall income structure

Short-term rentals (average stay under 7 days) are treated differently and may qualify under material participation standards even without Real Estate Professional Status.

This is where strategic planning…not just tax preparation…matters.

Seek Professional Advise

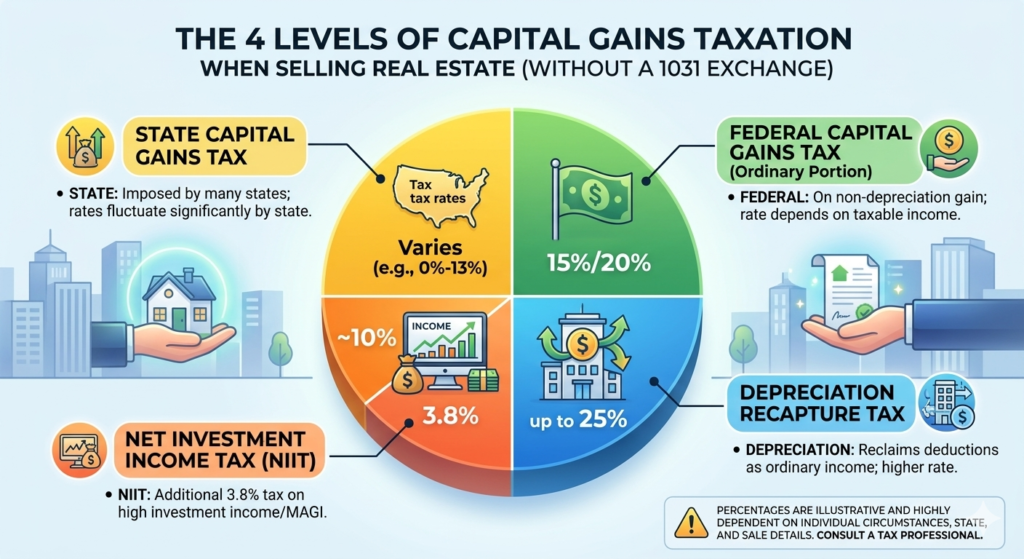

What About Recapture?

Accelerating depreciation increases early deductions, but if you sell the property, some depreciation may be recaptured.

However, recapture can often be mitigated through:

- 1031 exchanges

- Installment sales

- Strategic holding periods

- Estate planning (step-up in basis)

- Sale allocation planning

Cost Segregation is not a short-term gimmick. It is a long-term wealth planning tool.

The Often Overlooked Cost Segregation Benefit: Partial Asset Disposition

One of the most powerful aspects of Cost Segregation is rarely discussed.

When you replace:

- A roof

- HVAC system

- Flooring

- Structural components

You may be able to write off the remaining undepreciated value of the old component.

Without a Cost Segregation study, your CPA may not know how much that roof originally represented in the purchase price.

With proper documentation, you can remove the old asset from your books and deduct its remaining value.

Over a 10–20 year hold, this can be substantial.

Strategic Insight: Think Beyond the First-Year Deduction

Cost Segregation is not just about saving taxes in year one.

It is about:

- Improving capital efficiency

- Increasing reinvestment velocity

- Enhancing portfolio scaling

- Supporting 1031 planning

- Coordinating with estate and succession planning

Many Charleston investors are entering the later stages of their investing careers. Decisions today affect capital gains, estate transition, and long-term liquidity.

This is where tax strategy meets portfolio strategy.

“As a Real Estate Wealth Advisor, my role is not just to help you buy or sell property, but to help you understand how each decision fits into your long-term plan.“

Frequently Asked Questions About Cost Segregation

Yes. It is an IRS-recognized methodology supported by decades of tax court precedent and audit technique guidelines.

No. You can often perform a study retroactively (generally within 10–15 years) without amending prior returns.

No more than any other legitimate deduction. Proper documentation provided by an engineer’s report supporting the study are critical.

Typically $200,000+ purchase price for best efficiency, though some lower-value properties may qualify.

No. You still depreciate the remaining 70% (or similar portion) over 27.5 or 39 years.

You may face depreciation recapture, but strategic planning (including 1031 exchanges) can mitigate this.

Often yes—especially if you materially participate. These can be powerful candidates.

No. Coordination with your CPA is essential.

Cost Segregation Conclusion

Cost Segregation in the Charleston Area is not a shortcut. It is a planning decision.

When applied thoughtfully, it can:

- Improve early cash flow

- Reduce current tax exposure

- Support acquisition strategy

- Enhance long-term portfolio performance

The key is alignment. Your tax strategy should match your investment horizon, liquidity needs, and exit planning.

If you would like to evaluate whether Cost Segregation fits your Charleston investment portfolio, I invite you to schedule a strategy session. We will look at your property, your income structure, and your long-term goals, before making any recommendations.

Thoughtful planning always outperforms rushed decisions.

Authors

Bill Byrd and Waverly Byrd bring deep real estate expertise to clients throughout the Charleston area, drawing on years of hands-on experience with residential sales, investment property, relocation, and local market strategy. Their guidance is grounded in market knowledge, careful analysis, and a commitment to helping clients make well-informed real estate decisions.

As a father-and-daughter team, they work collaboratively on every transaction, combining experience, perspective, and consistent communication. Clients benefit from a coordinated approach that emphasizes preparation, clarity, and thoughtful execution at each stage of the buying or selling process across the Lowcountry.