A Guide for Real Estate Investors Planning their Next Stages of Life

How should real estate investment strategy change as investors reach their 60s, 70s, and 80s?

Real estate investors often benefit from adjusting their real estate investment strategy as they age. During their 50’s and 60s, many investors optimize their portfolio for appreciation and cash flow. In their 60’s and 70s, they often simplify and stabilize income by minimizing risk and consolidation. By their 70’s and 80s, the focus typically shifts toward preserving their accumulated wealth and preparing their assets for future transfer heirs and or legacy creation.

Introduction to The Evolving Real Estate Investment Strategy

Investing in Real estate has been one of the most popular alternative investments for many years. Prudent real estate investors have created significant wealth over the past several decades. However, strategies that worked well at age 40 may not serve the same purpose when investors reach the ages of 60, 70 or 80.

Over time, priorities often evolve. Investors may begin thinking about retirement income, reduced management responsibilities, tax exposure, and the long-term future of their properties. Therefore, reviewing a portfolio through the lens of ones life stage becomes an important exercise.

At Byrd Property Group, we regularly help property owners analyze their real estate holdings so they can make informed decisions about the next chapter of their investment strategy. In many cases, the conversation is not about selling real estate and cashing out. Instead, it focuses on determining whether the properties someone owns today remain the best assets for their portfolio for the years ahead.

Understanding how investment priorities shift during different decades can help investors approach these decisions with clarity and confidence.

Real Estate Investment Strategy in Your 60s: Portfolio Optimization

During their 60s, many investors begin shifting from acquisition mode to optimization mode.

At this stage, many investors still have a long investment horizon. However, they may start evaluating whether each property is performing as effectively as possible.

Key Questions to Ask at Age 60

Investors often benefit from asking themselves several important questions:

- Would I buy this property again today?

- Is this property producing strong income relative to its value?

- What type of income stream is considered optimal?

- Does the property require significant maintenance or management?

- How much equity is tied up in this asset?

- Does this property align with my future lifestyle goals?

These questions will help an investor reveal whether certain properties will continue to support their long-term financial goals. And more importantly, which properties may not be worth continueing to hold.

Portfolio Optimization Strategies

Several real estate investment strategies may help improve portfolio performance during this decade.

1. Conduct an Asset Performance Test

Some properties generate strong returns, while others quietly underperform. A detailed review can help identify which assets deserve long-term placement in the portfolio.

2. Consider Strategic Repositioning

In some cases, investors exchange or reposition properties to improve income, reduce management demands, or consolidate holdings.

For example, investors may:

- Use a 1031 exchange to defer taxes and exchange several smaller properties for one larger asset

- exchange a fully depreciated property to reset your depreciation schedule

- reposition an older home that will require frequent repairs

- shift toward properties that produce either greater or more consistent income

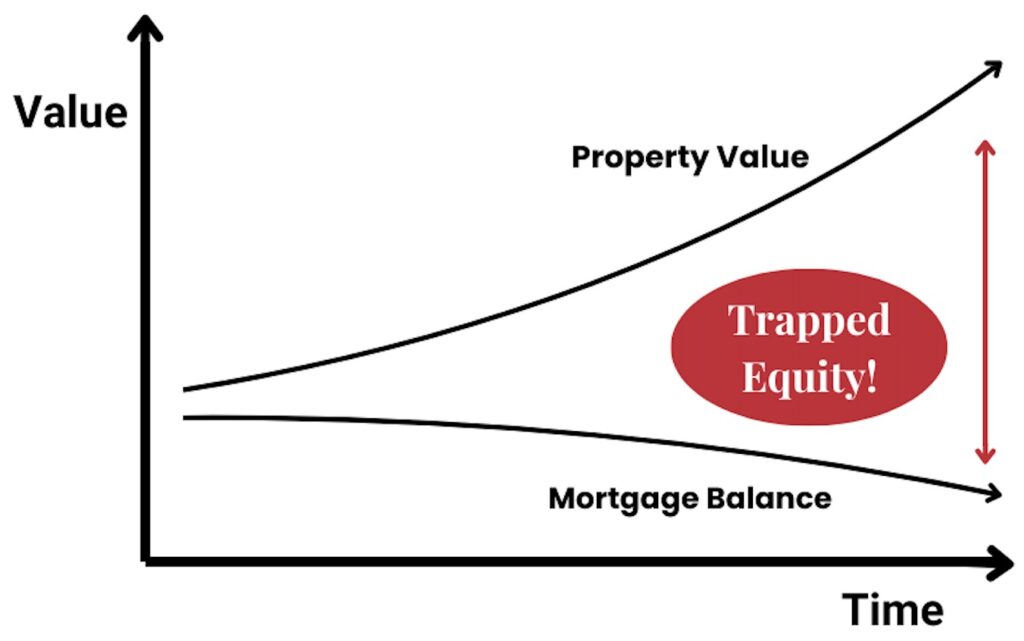

3. Evaluate Equity Efficiency

Over time, appreciation can create large amounts of trapped equity. Therefore, reviewing how efficiently that equity performs becomes extremly important.

Many of our investor clients find that having us run an Asset Performance Test provides valuable insights into this question.

4. Estate Planning Strategies

If an investor hasn’t started their estate plan, it’s not to early to start at this stage. At a minimun you should have a will and a funded trust in place. The last thing you want to put your family through is probate.

The two biggest enemies to wealth creation and family harmony are: Capital Gains Tax and when a real estate investor dies without a will and a funded trust and forces the family to endure probate.

Asset Performance Test or Capital Gains Analysis Page

Real Estate Investment Strategy in Your 70s: Income Stability and Simplicity

By their 70s, investors often begin prioritizing reliability and simplicity.

Many portfolios were built during decades of active investing. However, managing multiple properties can eventually require more time and attention than investors prefer.

Therefore, the goal during this stage often becomes maintaining income while reducing complexity.

Questions Investors Often Ask Themselves at Age 70

• Does this property generate dependable income?

• Does it require frequent repairs or tenant turnover?

• Would I want to manage this property ten years from now?

• Would my spouse or family be comfortable overseeing this asset?

These questions help determine whether the current portfolio still fits the investor’s lifestyle.

Strategies Investors May Consider in Their 60’s or 70’s

1. Portfolio Consolidation

Some investors reduce the number of properties they manage. For example, a portfolio of several single-family homes may be simplified into fewer assets.

Reducing the number of properties often reduces administrative responsibilities, maintenance coordination, and tenant management.

2. Professional Management

Hiring experienced property management can also help reduce day-to-day involvement.

When self manage your properties, you can look at the amount you would pay a property manager and consider that your W-2 wage for doing the job! Then decide, “is it worth it”? At a later stage of life, probably not!

3. Tax Planning

At this stage, tax exposure becomes an important consideration. Investors often evaluate strategies to manage capital gains, depreciation recapture, and income planning. Talk to your CPA, Financial Planner, Attorney and Real Estate Wealth Advisor and make sure you are 100% clear about how taxes will affect your real estate.

Real Estate Investment Strategy in Your 80s: Preservation and Legacy Planning

By the time real estate investors reach their 80s, priorities often shift again. At this stage, many investors focus on preserving wealth and preparing assets for future transfer.

This does not necessarily mean selling properties. Instead, the focus often becomes simplifying ownership structures and ensuring that heirs understand how assets are managed.

Important Questions Investors Consider

• Would my heirs want to manage these properties?

• Do they understand how these assets operate?

• Would fewer properties simplify future transitions?

• Do I have estate planning structures in place?

Answering these questions can help families avoid confusion later.

Estate Planning Considerations

Some investors explore planning strategies such as:

• family LLC structures

• living trusts

• coordinated estate planning with legal and tax professionals and more importantly their real estate wealth advisor.

In many cases, real estate offers important tax advantages when assets transfer between generations.

The Hidden Issue Many Investors Discover: Cap Rate

One concept that becomes especially important as investors age is a properties Cap Rate.

Over time, property values here in Charleston have risen dramatically. However, rental income in many areas has increased at a slower pace.

As a result, an investor might own a property worth $1,000,000 that generates $30,000 in annual income. While that income remains helpful, it represents only a 3% return or Cap Rate on the property’s current value.

Therefore, many investors benefit from periodically reviewing an Asset Performance Test to learn how their equity is currently performing within their portfolio.

This analysis does not always lead to selling a property. However, it often provides valuable insight into how each asset contributes to long-term financial goals.

The Life-Stage Portfolio Test

One simple framework can help investors think about their portfolio in a new way.

| Age | Portfolio Question | Strategic Focus |

|---|---|---|

| 50-60 | Would I buy these properties again today? | Optimization |

| 60-70 | Would I want to manage these assets in retirement? | Simplification |

| 70-80 | Would my heirs want to inherit these properties? | Legacy Planning |

This simple exercise often leads to meaningful conversations about long-term strategy.

Why Portfolio Reviews Matter

Many investors spend decades acquiring properties. However, they rarely revisit the portfolio with a long-term planning perspective.

Markets change. Neighborhoods evolve. Maintenance demands increase, tax and insurance costs rise and more. Meanwhile, personal goals also shift.

Because of these factors, periodic portfolio reviews can help investors ensure their real estate continues supporting their financial objectives.

At Byrd Property Group, our team regularly works with property owners in many states who want a thoughtful evaluation of their holdings. These conversations often involve reviewing income potential, equity performance, and long-term planning goals.

The objective is not to encourage unnecessary transactions. Instead, the goal is to provide clear information so investors can decide what makes sense for their next stage of life.

Planning the Next Chapter of Your Real Estate Portfolio

Real estate can remain an important part of a long-term financial strategy well into retirement years. However, thoughtful planning helps ensure that properties continue serving the investor rather than becoming a burden.

Some investors choose to keep their properties for income. Others simplify their portfolio. Still others reposition certain assets while holding others.

Each situation is unique.

If you own investment real estate in the Charleston area or elsewhere and are thinking about the next stage of your investment strategy, our team would be glad to help you explore your options.

Frequently Asked Questions

Many investors begin evaluating their portfolio in their early 50’s and 60s. At this stage, optimization and long-term planning become increasingly important.

Not necessarily. Some investors continue owning rental properties for income. Others simplify their holdings or reposition certain assets. The right strategy depends on individual financial goals and lifestyle preferences as well as the investors health.

Return on equity measures how much income a property produces compared to its current market value. This metric helps investors evaluate how efficiently their equity performs.

As investors age, priorities often shift toward income stability and reduced management responsibilities. Reviewing the portfolio helps determine whether existing properties still align with these goals.

An Asset Performance Test that analyzes property income, expenses and today’s value can help investors understand how their asset is performing against other investments.. Many investors benefit from a professional portfolio evaluation.

Authors

Bill Byrd and Waverly Byrd bring deep real estate expertise to clients throughout the Charleston area, drawing on years of hands-on experience with residential sales, investment property, relocation, and local market strategy. Their guidance is grounded in market knowledge, careful analysis, and a commitment to helping clients make well-informed real estate decisions.

As a father-and-daughter team, they work collaboratively on every transaction, combining experience, perspective, and consistent communication. Clients benefit from a coordinated approach that emphasizes preparation, clarity, and thoughtful execution at each stage of the buying or selling process across the Lowcountry.