Why should Charleston area investors start Building a Real Estate Plan instead of simply owning rental property?

Building a Real Estate Plan helps you treat your investment property as part of your broader financial, tax, retirement, and estate strategy. Instead of only collecting rent and hoping the property appreciates, a real estate plan helps you measure performance, understand tax exposure, evaluate 1031 exchange options, and decide whether the asset still fits your long-term goals.

Introduction

Building a Real Estate Plan is one of the most important steps a Charleston area real estate investor can take before retirement, before a major life event, or before family members are left to make decisions without a clear strategy.

If you own a rental home, land, second home, or other investment property, that real estate may represent one of the largest assets in your financial life. But many investors still treat it like “the house with a tenant” instead of part of a larger financial, retirement, tax, and estate plan.

In the Charleston area, where many properties have appreciated significantly over time, this can create both opportunity and risk. Your property may have grown in value, but that does not automatically mean it is still producing the best return, serving your retirement goals, or preparing your family for a smooth transition.

A thoughtful real estate plan helps you look at the property the way your financial advisor looks at your investment portfolio: with strategy, measurement, risk management, tax awareness, and long-term purpose.

Why Building a Real Estate Plan Is Different From Simply Owning Rental Property

Many residential real estate investors start the same way.

You buy a property. Then you rent it out. You repair it when something breaks and you hope the property appreciates. Someday, you may sell it, use the equity, pass it to your family, or let your heirs figure it out later.

That may work for a while, but it is not the same as Building a Real Estate Plan.

Owning rental property is about possession.

Building a real estate plan is about strategy.

A rental property without a plan often becomes:

- A house with a tenant

- A source of occasional income

- A repair responsibility

- A future tax problem

- A family decision waiting to happen

- An asset that may or may not still fit your goals

A real estate plan gives that property a job.

It helps you answer:

- Is this property still worth holding?

- Is the income strong enough compared to the equity?

- Are repairs, insurance, taxes, or management issues changing the equation?

- Would a sale or 1031 exchange create better options?

- How does this property fit into retirement?

- What happens to this asset if you become ill or pass away?

- Will your family know what to do with it?

That is the difference between being a landlord and managing real estate wealth.

A Real Estate Plan Gives Your Investment Property a Clear Strategy

A tenant does not automatically make a property a good investment.

A rental property can be occupied and still underperform. It can appreciate in value and still produce a weak return on equity. It can create income while also creating stress, liability, tax exposure, and estate planning problems.

That is why Building a Real Estate Plan starts with one basic question:

What is this property supposed to do for you now?

The answer may change over time.

At one stage of life, the goal may be growth.

At another stage, it may be income.

Later, it may be preservation, simplicity, tax planning, or family transition.

Your real estate investment strategy should reflect your current goals, not just the reason you bought the property years ago.

A clear real estate plan may help you decide whether to:

- Keep the property as-is

- Improve the property

- Raise rents or adjust management

- Refinance

- Sell and pay the tax

- Sell through a 1031 exchange

- Exchange into a lower-maintenance asset

- Reposition into more passive real estate

- Prepare the asset for heirs

- Coordinate the property with your estate plan

The goal is not to rush into a sale. The goal is to make the property serve the larger plan.

How Building a Real Estate Plan Mirrors Financial Portfolio Rebalancing

Most investors understand the importance of reviewing stocks, bonds, retirement accounts, and other paper assets.

A financial advisor does not usually buy a stock, ignore it for 25 years, and simply hope it works out. Your financial advisor reviews the portfolio, compares it’s performance to other assets. They consider risk, allocation, income needs, tax issues, and the investor’s age.

As investors get older, financial advisors often reposition portfolios.

They may move from:

- Higher risk to lower risk

- Growth to income

- Concentration to diversification

- Volatility to stability

- Complexity to simplicity

- Accumulation to preservation

- Wealth building to wealth transfer

Real estate investors should think the same way.

A rental property that made sense at age 45 may not be the best fit at age 65, 70, or 80. The property may still be valuable, but the structure of ownership may need to change.

This is one of the biggest reasons Building a Real Estate Plan matters.

Your real estate should be reviewed, measured, and repositioned when your goals change, just like the rest of your financial portfolio.

Your Real Estate Investment Strategy Should Change as You Age

Real estate can be a powerful wealth-building asset. But as real estate investors grow older the responsibilities and risks begin to feel different as you age. It’s important to understand how your real estate investment strategy should change throught your life.

When you are younger, you may be more willing to handle:

- Tenant turnover

- Late-night maintenance calls

- Vacancies

- Repairs

- Contractor coordination

- Financing risk

- Property management issues

- Legal and liability concerns

- Major capital expenses

Later in life, those same issues may become more of a burden.

You may still want income and you still may still like real estate investments. You may still appreciate the tax advantages. But you may not want the same level of active involvement.

A real estate plan helps you decide whether the property should remain an active rental, be improved, sold, exchanged, consolidated, diversified, or transitioned into a more passive form of ownership.

For senior real estate investors, the question is not just:

“Is the property valuable?”

The better question is:

“Does this property still fit the life I am trying to build now?”

Why a Charleston Area Real Estate Plan Matters for Long-Term Investors

The Charleston area creates a unique planning challenge for real estate investors.

Many long-term owners in Charleston, Johns Island, James Island, West Ashley, Mount Pleasant, Summerville, North Charleston, Wadmalaw Island, Kiawah, Seabrook, and surrounding communities have seen meaningful appreciation over time.

That appreciation can be a major benefit.

But it can also create planning issues, including:

- Large unrealized capital gains

- Depreciation recapture exposure

- More equity trapped in one property

- Lower return on equity

- Higher insurance costs

- Higher repair costs

- Increased property taxes

- More expensive maintenance

- Greater estate planning complexity

A Charleston area property may be worth far more than it was years ago. But if income has not kept pace with value, your return may be weaker than you think.

This is why Building a Real Estate Plan in the Charleston area should include more than a simple opinion of value.

You need to know how the property is performing, what tax exposure exists, what risks are increasing, and what options you may have before a major life event forces a decision.

A Real Estate Plan Should Measure Performance, Not Just Appreciation

Many investors focus on one number:

What is the property worth?

That number matters, but it is not enough.

A property can appreciate and still become inefficient. It can have a strong market value but weak income. It can look successful on paper while creating low return on equity.

For example, suppose you bought a rental property years ago for $250,000 and it is now worth $650,000.

That may be a very successful investment from an appreciation standpoint. But if the property only produces modest net income after taxes, insurance, repairs, vacancy, management, and maintenance, your current return on equity may not be very strong.

That does not mean the property was a mistake.

It may have been an excellent investment.

But Building a Real Estate Plan requires a better question:

Is this property still the best use of the equity today?

That question is especially important for long-term Charleston area investors who may have significant equity tied up in one or more rental properties.

Paper Assets Have Metrics. Your Real Estate Plan Should Too.

In the paper asset world, investors use metrics.

Financial advisors may look at:

- Price-to-earnings ratios

- Dividend yield

- Asset allocation

- Risk tolerance

- Portfolio performance

- Income needs

- Volatility

- Tax impact

- Time horizon

Real estate investors should also use metrics.

A strong real estate investment plan may review:

- Current market value

- Net operating income

- Cap rate

- Cash-on-cash return

- Return on equity

- Rent-to-value ratio

- Debt structure

- Vacancy risk

- Insurance trends

- Property tax trends

- Deferred maintenance

- Capital gains exposure

- Depreciation recapture

- Estate planning impact

- Management burden

Many residential investors know the rent and mortgage payment. They may know whether the property feels profitable.

But feeling profitable is not the same as measuring performance.

A real estate plan helps you move from guessing to evaluating.

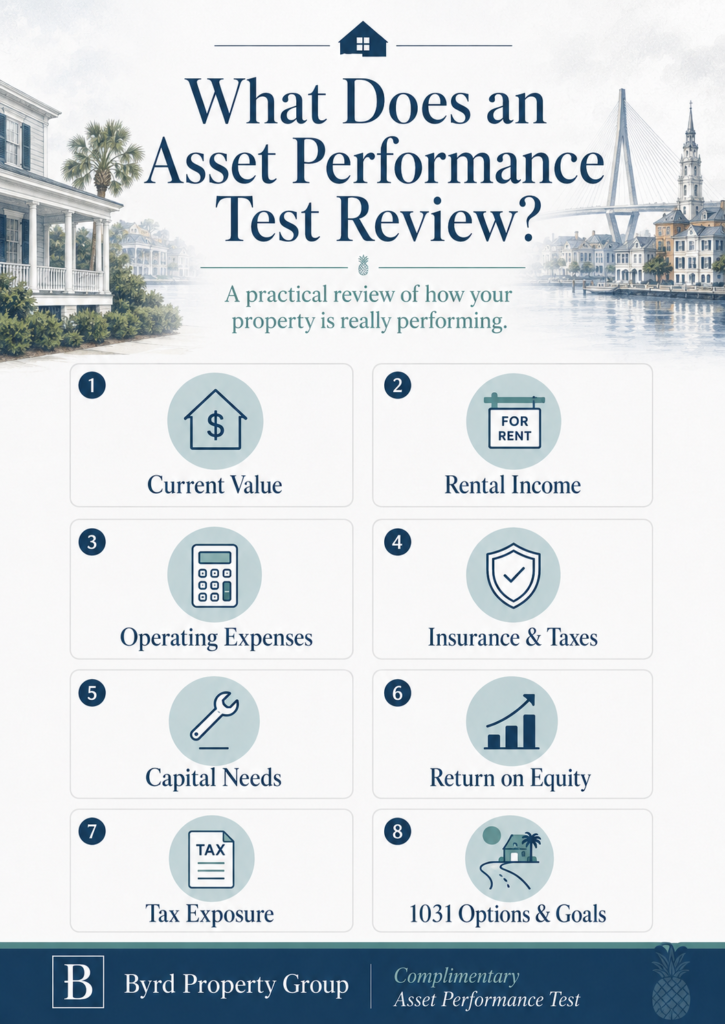

Why an Asset Performance Test Belongs in Your Real Estate Plan

An Asset Performance Test/Review is one of the most practical first steps in Building a Real Estate Plan.

It helps you evaluate your investment property more like a financial asset and less like a house you happen to rent out.

An Asset Performance Test may help you understand:

1. What the Property Is Worth Today

You need a realistic value range based on local market conditions, not just an online estimate.

This is especially important in the Charleston area, where property type, location, condition, flood zone, rental demand, insurance, and neighborhood trends can make a major difference.

2. How Much Equity Is in the Property

Equity is valuable, but it also needs to be evaluated.

If a large amount of equity is producing a small amount of income, the property may be underperforming.

3. What the Property Is Truly Producing

Gross rent does not tell the full story.

You need to consider:

- Repairs

- Vacancy

- Taxes

- Insurance

- HOA fees

- Management

- Maintenance reserves

- Capital improvements

- Debt service

Net income is what matters.

4. What Your Return on Equity Looks Like

Return on equity helps you compare the property to other possible uses of the capital.

This does not mean you should automatically sell. It simply helps you understand whether the current asset is still working efficiently.

5. What Risks Are Increasing

Risk can come from many places:

- Aging HVAC systems

- Roof condition

- Insurance increases

- Tenant turnover

- Deferred maintenance

- Local market changes

- Financing issues

- Legal exposure

- Storm and flood considerations

A real estate plan should account for these risks before they become urgent.

6. Whether the Property Still Fits Your Stage of Life

A property that was once a good fit may no longer match your current needs.

That is not a failure. It is simply a reason to review your options.

7. What Repositioning Options May Exist

After reviewing performance, you may consider:

- Holding

- Improving

- Refinancing

- Selling

- Exchanging

- Consolidating

- Diversifying

- Moving toward more passive ownership

- Preparing the property for transfer

The Asset Performance Test gives you a clearer picture before you decide.

Why Capital Gains Planning Should Be Part of Your Real Estate Plan

Many investors avoid reviewing their options because they are concerned about taxes.

That concern is understandable.

If you have owned a Charleston area investment property for many years, your taxable gain may be significant. But not knowing the number does not make the issue go away.

Understanding Capital Gains should be part of your real estate plan because it helps you estimate what may happen if you sell.

A capital gains review may include:

- Original purchase price

- Major improvements

- Depreciation taken

- Current estimated value

- Selling costs

- Debt payoff

- Potential capital gain

- Depreciation recapture

- State tax considerations

- Federal tax considerations

- Possible 1031 exchange options

- Estate planning considerations

This is not a substitute for advice from your CPA, tax advisor, or attorney.

But it gives you a better starting point.

Before you make a decision about selling, exchanging, holding, or transferring a property, you should understand the possible tax impact.

That is a core part of Building a Real Estate Plan.

How 1031 Exchanges Fit Into Building a Real Estate Plan

A 1031 exchange can allow an investor to sell qualifying investment property and reinvest into other qualifying real estate while deferring capital gains taxes, provided the IRS rules are followed.

But a 1031 exchange is not just a tax strategy.

For many investors, it is a repositioning strategy.

That is why 1031 planning often belongs inside a larger real estate investment plan.

Investors may use a 1031 exchange to:

- Move from high-maintenance property to lower-maintenance property

- Exchange one property for multiple properties

- Consolidate several properties into one stronger asset

- Shift from active management to more passive ownership

- Move from low income to stronger income potential

- Diversify by location or asset type

- Reduce tenant and repair headaches

- Prepare for retirement income

- Preserve more equity for reinvestment

- Improve estate planning flexibility

This is similar to what a financial advisor does when adjusting a paper portfolio.

You are not necessarily leaving real estate. You are changing the structure of your real estate ownership to better fit the next phase of life.

Real Estate Plan Examples for Charleston Area Investors

The right strategy depends on your property, goals, age, tax situation, and family needs.

Here are several examples of how Building a Real Estate Plan may help a Charleston area investor think more clearly.

Example 1: Repositioning an Aging Rental Property

You may own an older rental house with strong appreciation but rising repair costs.

The property may still rent, but the roof, HVAC, insurance, taxes, and maintenance needs are becoming more expensive.

An Asset Performance Test may show that your return on equity is lower than expected.

Your real estate plan may include:

- Holding and improving the property

- Adjusting rent

- Changing management

- Selling and paying the tax

- Using a 1031 exchange to reposition

- Moving into a lower-maintenance asset

The best answer depends on the numbers and your goals.

Example 2: Moving From Active Landlord to More Passive Ownership

Some investors reach a point where they still want real estate income but no longer want the landlord responsibilities.

They may not want calls from tenants, contractors, or property managers.

A real estate plan may help them evaluate whether a 1031 exchange into a more passive real estate structure could fit their retirement goals.

This may be especially relevant for older landlords who want income, simplicity, and less day-to-day involvement.

Example 3: Reducing Concentrated Real Estate Risk

A family may own one highly appreciated rental property that represents a large percentage of their net worth.

That creates concentration risk.

If the property has a major repair, vacancy, insurance issue, tenant problem, storm damage, or market shift, the family’s financial picture may be affected.

A real estate plan may consider whether to:

- Keep the property

- Sell and diversify

- Exchange into multiple properties

- Shift into a different asset type

- Coordinate with the family’s broader financial plan

The purpose is to avoid having too much of the family’s wealth dependent on one property.

Example 4: Preparing Real Estate for the Next Generation

Many owners assume their children will simply figure out what to do with the property later.

That can create unnecessary stress.

One child may want to keep it. Another may want to cash it out to cover some personal need or want. One child may live out of state and may not want management responsibility.

Building a Real Estate Plan helps you think through Senior Living Options and the transition before your family has to make decisions during a difficult time.

How Estate Planning Connects to Your Real Estate Plan

Real estate is often one of the largest assets in a family’s financial life, but it is not always fully integrated into the estate plan.

Your will or trust may say who receives the property. But that does not always mean the asset is positioned well.

A real estate plan should consider:

- How the property is titled

- Whether ownership matches the estate plan

- Whether heirs understand the property’s value

- Whether heirs understand the tax issues

- Whether there is debt on the property

- Whether there is deferred maintenance

- Whether the property is easy or difficult to sell

- Whether family members have different financial needs

- Whether a sale, hold, exchange, or transfer makes sense

- Whether your advisors have coordinated around the property

This is where your real estate advisor, CPA, attorney, and financial advisor should be part of the same conversation.

The goal is not just to transfer an asset.

The goal is to transfer it thoughtfully.

Why “I’ll Deal With It Later” Can Hurt Your Real Estate Plan

Many real estate investors wait until something happens.

That trigger may be:

- A medical situation

- Retirement pressure

- A death in the family

- A major repair

- A tenant problem

- A sudden need for cash

- A tax deadline

- A family disagreement

- A market shift

At that point, options may be limited.

Being proactive and building a Real Estate Plan before an unexpected event comes up gives you more control.

- You can evaluate the property at your leisure without pressure.

- Estimate taxes.

- Talk with your CPA.

- Consider a 1031 exchange.

- Prepare the property for a sale.

- You can involve your family.

- You can coordinate with your financial planner and your estate plan.

Waiting does not always cause harm, but it often narrows your choices. It’s better to make the decisions yourself, then have them made for you!

Strategic Insight: Building a Real Estate Plan Means Managing Real Estate Wealth, Not Just Selling Property

This is where the role of a Real Estate Wealth Advisor is different from a traditional transaction-focused real estate agent.

A transaction agent helps when you are ready to buy or sell.

A strategic real estate advisor helps you evaluate whether the property still fits your plan before the transaction decision is made.

That means looking at:

- Market value

- Income performance

- Equity position

- Tax exposure

- Lifestyle impact

- Risk

- Retirement goals

- Family transition

- 1031 exchange options

- Estate planning concerns

- Coordination with your CPA, attorney, and financial advisor

Potential Decisions

- Maybe sell.

- Maybe to hold.

- Or exchange.

- It may be to improve the property.

- Or you could simply adjust rent or management.

- It may be to prepare the asset for your heirs.

The point is not to push one answer.

The point is to build a clear plan.

That is what Building a Real Estate Plan is really about.

A Simple Framework for Building a Real Estate Plan

If you own investment property in the Charleston area, here is a practical framework to begin.

Step 1: Define the Property’s Purpose

Ask yourself what the property is supposed to do now.

Is the goal:

- Current income?

- Long-term appreciation?

- Retirement income?

- Tax deferral?

- Wealth preservation?

- Family legacy?

- Future liquidity?

- Diversification?

- A possible 1031 exchange?

- A future sale?

If you cannot clearly define the purpose, the property may be operating without a real strategy.

Step 2: Measure Current Performance

Review the numbers.

You should understand:

- Rent

- Vacancy

- Repairs

- Taxes

- Insurance

- HOA fees

- Management fees

- Debt service

- Net income

- Current value

- Estimated equity

- Return on equity

This step helps turn the property from a vague asset into a measurable investment.

Step 3: Review Tax Exposure

Before you sell, exchange, gift, or transfer property, estimate the tax impact.

This is where a Capital Gains Assessment can help prepare you for a better conversation with your CPA or tax advisor.

Step 4: Compare Your Options

After you understand value, income, equity, risk, and taxes, you can compare your choices.

Your options may include:

- Hold the property as-is

- Improve the property

- Adjust rent or management

- Refinance

- Selling your rental property or keep it

- Use a 1031 exchange

- Exchange into a lower-maintenance asset

- Exchange into multiple assets

- Move toward passive ownership

- Prepare the property for estate transition

Step 5: Coordinate With Your Larger Financial Plan

Your real estate plan should connect with your:

- Financial plan

- Retirement income plan

- Tax plan

- Estate plan

- Insurance plan

- Family goals

Real estate should not sit outside the planning conversation.

For many Charleston area investors, it may be one of the most important parts of that conversation.

Frequently Asked Questions About Building a Real Estate Plan

Building a Real Estate Plan means evaluating your investment property as part of your broader financial, retirement, tax, and estate strategy. It includes reviewing value, income, equity, risk, capital gains exposure, 1031 exchange options, and long-term family goals.

Charleston area investors often own properties that have appreciated significantly over time. That appreciation can create opportunity, but it may also create tax exposure, trapped equity, insurance concerns, estate planning issues, and lower return on equity. A real estate plan helps you evaluate those issues before making a major decision.

No. A rented property may still be underperforming. You need to review net income, expenses, equity, return on equity, repair risk, tax exposure, and management burden. A tenant provides rent, but that does not automatically mean the asset is being used well.

Financial advisors review and reposition paper assets as clients age. Real estate investors should do the same with rental properties, land, and other investment real estate. Your real estate investment strategy should adjust as your goals, risk tolerance, tax situation, and retirement needs change.

An Asset Performance Test is a review of how your investment property is performing today. It may include market value, rent, expenses, net income, equity, return on equity, maintenance risk, and repositioning options. It helps you decide whether to hold, sell, improve, exchange, or transition the property.

A Capital Gains Assessment helps estimate the potential tax impact of selling an investment property. It can help you prepare for conversations with your CPA, tax advisor, or attorney and determine whether a 1031 exchange or another strategy may be worth considering.

A 1031 exchange may allow you to sell qualifying investment property and reinvest into other qualifying real estate while deferring capital gains taxes. In a real estate plan, a 1031 exchange may be used to reposition into lower-maintenance, more diversified, more income-focused, or more retirement-friendly assets.

No. Building a Real Estate Plan does not mean you have to sell. The right answer may be to hold, improve, refinance, exchange, sell, or prepare the property for your heirs. The purpose is to understand your options before you are forced to make a decision.

Conclusion

Your Charleston area investment property may be much more than a rental house.

It may be part of your retirement plan, tax picture, estate plan, family legacy, and long-term financial security.

The question is whether it is being managed that way.

Building a Real Estate Plan gives you a clearer view of your property’s value, income, equity, risk, tax exposure, and future options. It helps you decide whether to hold, sell, exchange, improve, refinance, or prepare the asset for a smoother transition.

You do not need to make a rushed decision. But you should not wait until a medical issue, family transition, major repair, or tax deadline forces the decision for you.

If you own investment property in the Charleston area, start with a thoughtful review. An Asset Performance Test and Capital Gains Assessment can help you see whether your real estate is still working for your larger financial plan.

About the Authors

Bill Byrd and Waverly Byrd serve clients throughout the Charleston area as Real Estate Wealth Advisors, helping individuals and families navigate complex property decisions connected to life transitions and long-term planning. Their work often involves, tax-advantaged 1031 exchanges, probate and estate property sales, divorce-related real estate solutions, trusts, and senior relocation, situations where informed coordination and careful timing can significantly impact outcomes.

With decades of experience, Bill and Waverly emphasize education, clarity, and collaboration. They regularly work alongside financial planners, tax professionals, and attorneys to help clients understand their options and align real estate decisions with broader financial and estate planning goals. As a father-and-daughter team, they guide clients through sensitive transactions with discretion, organization, and a steady, well-informed approach across the Lowcountry.